Less than a quarter of an hour after opening, the Chinese stock market was closed by an automatic shutdown. This was triggered twice last week by rapid falls of more than 7%. This "circuit-breaker" mechanism was imposed by the government only 5 months ago after equally dramatic losses. The government has now suspended this measure, not from new-found confidence, but as a further turn of panic.

Already this week the market has fallen 5% in one day. Falls in the Shanghai and Shenzhen stock exchanges took their losses so far this year to 15% and 20%, respectively. The installation of this circuit-breaker reveals how nervous the Chinese government is of the underlying economic instability.

The slowdown of the Chinese economy has been an established fact for some time now, and is known as a major cause of the recession in Brazil and slowdowns in many economies such as Australia, as well as the sustained collapse in commodity prices in the world market. The extreme turbulence of the stock market is an omen of a very "hard landing" for the real economy, exposing the mountains of debt and contradictions the long boom has built up.

Prior to this and last week’s stock market crashes the real economy had already ushered in 2016 with bad news. The manufacturing sector, the heart of the Chinese economy and the world’s largest, shrank for the fifth month in a row in December, marking 9 months of overall decline. The decline is so undeniable that even the National Bureau of Statistics, notorious for "cooking the books" to deliver good news, said that “financial tensions had become 'more prominent' toward the end of the year and 'the downward pressure on manufacturing was still relatively big'.” ( Financial Times, 1.1.16). There is no doubt that the slowdown is real.

Nevertheless, it is common for journalists to take succour from the secondary and semi-fictitious character of the Chinese stock market. It is routinely pointed at that Chinese stocks represent a small portion of Chinese capital; their flightiness representing precisely their disconnection from the more sound fundamentals of the economy. It is certainly true that the Chinese stock market is much less integral to Chinese capitalism than the Dow Jones is to the US, and this volatility is for that reason unlikely to directly cause a financial and economic crisis.

But stock markets are also barometers for the health of an economic system. When and where growth has become unsound and overstepped the limits set by capitalism, we tend to see bubbles, distortions and imbalances in all kinds of strange places. The flightiness of the Chinese stock market may not directly represent the economy as a whole, but is a symptom of the imbalance of the economy as a whole. That its huge rise a year ago, and its subsequent crash, were exaggerated, fictitious, removed from economic reality, is not a healthy thing and is evidence of the chronic overproduction stored up in the real economy.

Prior to this boom and crash of the stock market, we had the enormous debt fuelled property bubble, which also crashed. Both happened because investors lacked opportunities for profitable investment in manufacturing due to overproduction. Enormous overproduction in the Chinese economy has been a reality since the world crisis in 2008, which meant that the vast industrial expansion of China now lacked a viable market. Key Chinese industries such as steel are grotesquely over-extended.

As has been widely documented, in 2008 the Chinese government stared into the abyss and panicked. The resulting fiscal stimulus it launched was the biggest in world history and managed both to shield China from the crisis and to rescue the world from an out-and-out depression. But that has come at the cost of a future crisis that is now imminent. The fiscal stimulus was achieved by way of foisting debt onto state owned enterprises to keep the economy growing, resulting in an explosion of debt that must now be paid off. Indeed, the stimulus itself resulted in greatly diminishing returns. Six years ago “it took just over $1 of debt to generate $1 of economic growth in China. In 2013 it took nearly $4”, the reason being that with the accumulation of unpaid debts “one-third of the new debt now goes to pay off old debt.” ( Financial Times, 27.1.14) The Chinese economy has become clogged up with unproductive debts because the government-led debt stimulus could not be used sufficiently for productive investment. Why take on debt to invest in new factories if the rest of the world economy is stagnant and demand is declining? Thus these new debts were used in short-sighted speculation instead. It is this underlying overproduction that has caused investors to speculate first in property, now in the stock market. The bursting of the stock market bubble reflects the unsoundness of this speculation, and in turn the unsoundness of the economy as a whole.

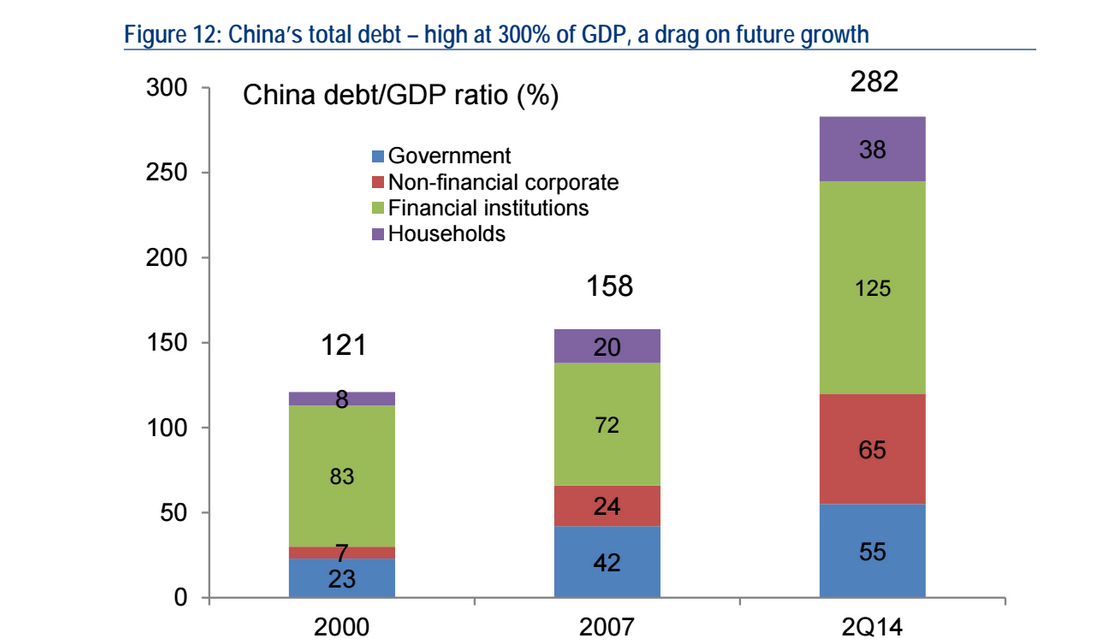

The statistics for the growth of debt in China are breathtaking. A year ago McKinsey and Co. produced data showing that total debt in the Chinese economy had quadrupled in only seven years to $28tn, 282% of GDP and 14% of the total global debt. China is addicted to debt. It cannot pay off the accumulated debts, many of which are in reality non-performing loans, and has to borrow more just to pay off what it already has, not to increase production.

The statistics for the growth of debt in China are breathtaking. A year ago McKinsey and Co. produced data showing that total debt in the Chinese economy had quadrupled in only seven years to $28tn, 282% of GDP and 14% of the total global debt. China is addicted to debt. It cannot pay off the accumulated debts, many of which are in reality non-performing loans, and has to borrow more just to pay off what it already has, not to increase production.

The debt mountain is more chronic in certain industries, especially key ones such as commodities (i.e. raw materials). According to Macquarie, debt in this sector has increased by 300% since 2007, and about half of these companies now have interest payments that are twice as high as their earnings. These figures speak to a profound, intractable problem in the Chinese and world economies. Capitalism has hit its limits.

The slowdown in the economy, the big falls on the stock exchanges, and the government’s cack-handed attempt to manage this, are causing very significant capital flight from the Chinese economy. The currency (Yuan) has reversed its upwards trajectory and has started to fall quite dramatically. This time it is not the government artificially devaluing the currency to strengthen exports, on the contrary, the government is battling against strong market pressure to sell the currency. This is reflected in the lower price for Yuan traded offshore than in mainland China because in the former the government allows market forces more freedom. Today the two rates converged, but only thanks to governmental use of “ ‘nuclear strength’ weapons to deter an attack on the yuan by short sellers and convince sceptical investors that they are in control of the country’s spluttering financial system.” ( The Guardian, 12.1.16).

China is terrified that dramatic falls in its currency could be both caused by and a cause of massive capital flight from the economy, causing a recession. So it is burning through its substantial foreign exchange reserves to buy Yuan and artificially prop up its value. This has caused its official hard currency reserves to fall by 1/6th since June 2015 ( The Financial Times, 11.1.16). It is scrambling new capital controls to stem capital flight. George Magnus writes in the Financial Times that,

“It is in this context that we might reflect on the recent announcement of a $512bn fall in currency reserves in 2015. Since China has a current account and net direct investment surplus of about $600bn, implied capital outflows must have been close to $1tn. Some of this was capital flight. Given the interplay between capital flight, a more uncertain “managed” currency depreciation and a private credit binge that’s going in the wrong direction, China’s credit crisis may be approaching now just that little bit faster.” (The Financial Times , 11.1.16)

All of this shows that a full-blown financial and economic crisis in China is very much on the cards. That is extremely important for the perspectives for the world capitalist system, because in 2008 it was China’s dodging of the crisis that pulled up the world economy. The world economy remains plagued with the debt and overproduction that caused the last crisis (which is in reality ongoing). The 2008 crisis did not have the consolation of purging the world of debt and overproduction, indeed Asian and global levels of debt far from being paid off have only grown since then, as the following charts show.

So the world is extremely vulnerable to another financial crisis just as it becomes sick of austerity. Only this time the reserves of fat have been burned away, and China, the last bastion against an all-out depression in 2008, will not only not rescue the world this time, but will likely be the cause of its crisis. And the effect today of whatever happens in the Chinese economy is greater than in 2008 as its share of trade and production has only grown - this year it will account for 18% of the world economy.

So the world is extremely vulnerable to another financial crisis just as it becomes sick of austerity. Only this time the reserves of fat have been burned away, and China, the last bastion against an all-out depression in 2008, will not only not rescue the world this time, but will likely be the cause of its crisis. And the effect today of whatever happens in the Chinese economy is greater than in 2008 as its share of trade and production has only grown - this year it will account for 18% of the world economy.

The world economy is already feeling the effects. The Dow Jones Industrial Average has had its worst start to any year in its history, as has the S&P 500, which lost $864bn over four days. Oil prices are now down to $31 (from $147 a few years ago), and may fall as low as $10 a barrel! There are fears that a significant Chinese slowdown or recession could cause global deflation and debt defaults. Already 2015 witnessed the slowest world growth since the crisis in 2008/9. The Royal Bank of Scotland has just written to its clients urging them to "sell everything" except the highest quality bonds, because “the current situation [is] reminiscent of 2008, when the collapse of the Lehman Brothers investment bank led to the global financial crisis. This time China could be the crisis point.” ( The Guardian, 12.1.16)

The world economy is already feeling the effects. The Dow Jones Industrial Average has had its worst start to any year in its history, as has the S&P 500, which lost $864bn over four days. Oil prices are now down to $31 (from $147 a few years ago), and may fall as low as $10 a barrel! There are fears that a significant Chinese slowdown or recession could cause global deflation and debt defaults. Already 2015 witnessed the slowest world growth since the crisis in 2008/9. The Royal Bank of Scotland has just written to its clients urging them to "sell everything" except the highest quality bonds, because “the current situation [is] reminiscent of 2008, when the collapse of the Lehman Brothers investment bank led to the global financial crisis. This time China could be the crisis point.” ( The Guardian, 12.1.16)

For the Chinese regime, an economic crisis is also a deep political crisis. The government very explicitly rests its legitimacy on economic growth, rising living standards and general economic stability and competence. They are about to be found out. As their legitimacy crumbles, they fear more than anything else a rising of the working class, those hundreds of millions of toilers who have made, and continue to make, China the economic powerhouse it is.

The Chinese working class has been gaining in organisation, confidence and militancy for years. Strikes are growing all the time, and the latest figures show that not only did 2015 see a record number of strikes (double that of 2014), but that these strikes spiked dramatically in December, only one month ago.

Just as the economy is failing, which will force the Chinese capitalists to pile pressure, wage cuts and redundancies on the workers, the workers are at their most militant. The government can see the danger and is repressing leading trade union activists more than ever. According to the Financial Times

“ Chinese police have arrested four worker activists based in the country’s Guangdong manufacturing hub, according to lawyers, in what has been described as the harshest crackdown against organised labour by the Chinese authorities in two decades.

...

Cheng Zhenqiang, the lawyer representing Zeng Feiyang, one of the activists arrested on Friday, told the FT by telephone that it was clear China’s slowing economy was playing a role.

“Of course [the crackdown] is related to the economic downturn ” (Financial Times, 11.1.16)

The Chinese working class knows no life but one of heavy state repression. It has always been extremely dangerous for them to put their heads above the parapet. And yet they have learnt to defend themselves and win better wages. They are well aware that it is their toil and poverty wages that have made their ruling class the second most powerful in the world. The workers want what is rightfully theirs, that is, a decent life. The looming crisis threatens to remove any chance of that, and the workers will not accept this. The perspective for 2016 and beyond, in China and globally, is of deep economic crisis and irreconcilable class struggle.